Finding a floor - Cyber Insurance

The future of the global cyber insurance market

The first global Cyber report released by DUAL.

Read the highlights and download the full report.

Executive summary

Cyber insurance has reached a critical juncture. As a relatively young market with rising penetration, it has yet to follow the cyclical patterns seen in more mature classes.

Instead, it has moved rapidly through distinct phases: early exposure-led growth, a sharp pricing correction and, more recently, sustained softening. The extent of softening is now raising concerns that the market may be approaching a profitability floor, yet there is limited analysis of the choices that will determine what comes next. This report seeks to close that gap. Rather than focusing on prevailing conditions, it draws on proprietary insights across the US, Europe, the UK and Australia and New Zealand (ANZ) to set out a forward-looking path towards a more sustainable market – one that reduces the risk of a severe correction whilst supporting all participants across the value chain. With premiums under pressure, exposures expanding and the threat landscape remaining elevated, the next phase will determine the market’s trajectory. Our analysis uncovers the actions required to sustain a market that underpins resilience against an increasingly complex cyber threat landscape and reinforces the broader relevance of insurance.

Europe: the path to stability

The cyber insurance market in Europe is deep into the softening phase, with elevated capacity and intense competition driving sustained rate reductions and higher limits. Although capacity growth has slowed in recent months relative to the surge of the past two years, aggregate supply remains abundant and continues to exceed demand, even as first-time buyers enter the market and existing clients purchase higher limits. Competition remains high across Europe. Spain, Italy and France, where increased switching of insurers and brokers is driving more aggressive rate reductions, are currently the most competitive markets, followed by the Nordics and Benelux. Buyers in the DACH region (Germany, Austria and Switzerland) demonstrate comparatively stronger broker and insurer loyalty, contributing to more stable conditions and more moderate softening. Competitive conditions extended into 1Q26 renewals, where most portfolios saw rate decreases in the double-digit range. More substantial corrections (of up to 70-75%) were achieved on individual accounts that had not previously been repriced in line with broader market movements. Continued softening is expected through 2026. In the absence of a significant loss event, further rate reductions remain the most likely outcome, albeit at a gradually moderating pace. As compounded rate decreases compress margins, sustaining portfolio resilience and profitability is likely to take precedence over growth for some underwriters.

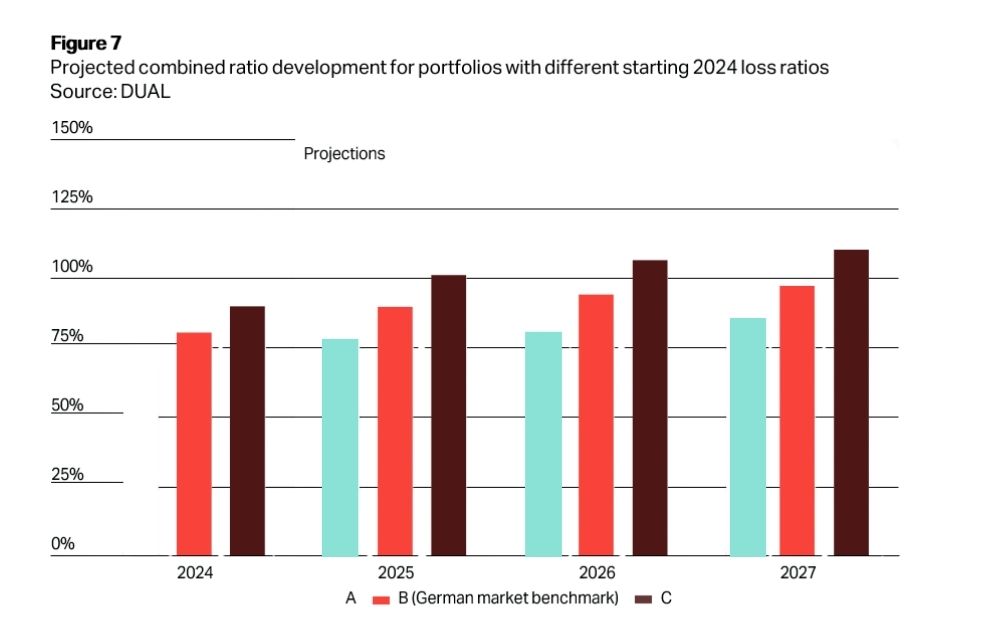

Although the underwriting performance of the European cyber market remains favourable overall, dispersion between carriers is significant. Whilst most portfolios retain meaningful margin buffers, others are materially closer to becoming unprofitable. DUAL research shows that tolerance for continued rate reductions depends heavily on existing portfolio performance. To assess sustainability, analysis has been applied to three representative cases: the GDV benchmark for the German market (45.5% starting loss ratio in 2024), a theoretical high margin portfolio (starting loss ratio of 35%) and a lower-margin portfolio (starting loss ratio of 55%).

In each case, a 35% expense ratio has been added to the starting loss ratio to derive the initial combined ratio. The scenarios incorporate observed rate reductions based on DUAL Europe data underlying Figure 3 (with 4Q25 and 1Q26 assumed to mark the point of peak softening), forward projections of decelerating rate declines through 2026 and 2027 and no major loss events. The results in Figure 7 show that the GDV benchmark (B) moves close to profitability thresholds by 2027 as margins compress. The high-margin portfolio (A) retains headroom to absorb further pricing pressure whilst the lower-margin portfolio (C) encounters profitability challenges this year.

Concurrent with pricing decreases, policy coverage across Europe has broadened. Over the past 12-24 months, some carriers have increased supply chain exposures by enhancing contingent business interruption terms and coverage extensions. Whilst responsive to client demand, these developments increase structural aggregation risk and raise the probability of correlated losses as coverage breadth expands. Supply chain exposure introduces underwriting challenges. Insurers are extending coverage to losses originating within third party networks beyond their (and often insureds’) visibility and control. The complexity of digital interdependencies increases the probability of correlated loss events across portfolios. Unlike ransomware, where underwriting standards and risk controls have matured considerably, systemic supply chain and technology-driven aggregation risks remain relatively untested. The lack of recent large-scale, correlated losses obscures the true severity potential. In a soft market, expanded coverage alongside lower pricing materially increases exposure to such systemic risks.

Two pathways are likely to emerge over the next 12-24 months. In the absence of a major loss, continued rate reductions through 2026 will compress margins and begin to decelerate as carriers approach profitability thresholds. Our combined ratio forecasts indicate that margin compression alone is likely to be sufficient to establish a pricing floor in 2027, as lower rates, broader coverage and signs of reduced underwriting discipline strain returns. The pace and impact of stabilisation will vary materially by portfolio. The alternative scenario, involving a systemic aggregation event or multiple smaller to medium-sized incidents generating widespread losses, would likely trigger rapid repricing, potentially accompanied by capacity withdrawal and renewed volatility. It is in both clients’ and underwriters’ interest that the market avoids another major correction. The challenge therefore now lies in managing competitive pressures without compromising the long-term sustainability of underwriting performance.

Our analysis shows that 2026 represents an inflection point for the cyber insurance market. After a period of sustained softening, margins will come under pressure for some carriers as pricing declines, exposures expand and the threat landscape remains elevated. Two paths now lie ahead. The first leads to gradual stabilisation over the next 12 months, supporting a sustainable market. The second sees softening continue this year and next, increasing the risk of a more severe correction. It is in clients’ interests that the market delivers the former. Underwriting expertise, portfolio resilience and long-standing relationships will determine which carriers are best positioned to navigate the next phase. Those with a proven ability to deliver consistent performance through different pricing environments will be better placed to support clients in a more complex risk environment. For our broking partners, this transition reinforces the importance of engaging with experienced, committed capacity providers. Securing stable, high-quality coverage will be critical as the market evolves. Cyber insurance continues to play a vital role in enabling resilience against an increasingly complex and interconnected threat landscape. Regardless of when and how quickly the market moves to a more disciplined phase, DUAL remains committed to delivering solutions that balance affordability, coverage and sustainable capacity

Ali Khodabakhsh, Head of Cyber Europe